By Ballo Ngomna & Joël Moudio (Download Pdf Version)

Diaspora Investors and Access to Bank Credit in Cameroon: Constraints and Opportunities

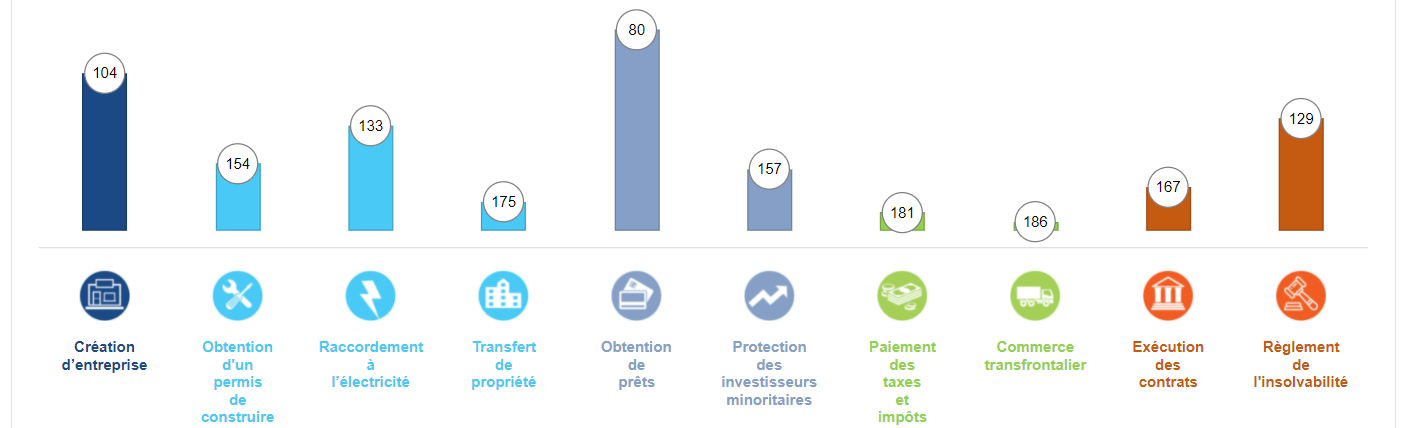

According to the Doing Business 2020 report, “compared to the previous year, sub-Saharan African economies improved their average score by 0.9 points” on the Doing Business index, which ranks countries on the ease of doing business. Overall, Cameroon’s index value (46.1) does not give it an honourable ranking (167th out of 190). However, its ranking is better in terms of obtaining loans (80th out of 190), one of the ten components used to calculate the index. This is the component where the country scored best (Figure 1).

Figure 1: Cameroon’s ranking in the ten areas of the Doing Business 2020 Index

Source: World Bank. 2020. Doing Business 2020. Economy Profile, Cameroon. Washington, DC: World Bank. CMR.pdf (doingbusiness.org) [Screenshot. Visited on 25 August 2021. Note: A higher ranking is indicated by a lower number and a higher bar. Thus, in the figure above, the top ranking is for obtaining loans, with a rank of 80. In terms of obtaining loans, together with Ghana, Cameroon has the highest ranking in sub-Saharan Africa (80th out of 190 in the world, and 13th in sub-Saharan Africa) with a score of 60 for both countries, well above the average for sub-Saharan Africa (45.2).

Table 1: Obtaining loans in Cameroon and the comparator economies

Source: World Bank. 2020. Doing Business 2020. Economy Profile, Cameroon. Washington, DC: World Bank. CMR.pdf (doingbusiness.org) [Visited on August 25, 2022]

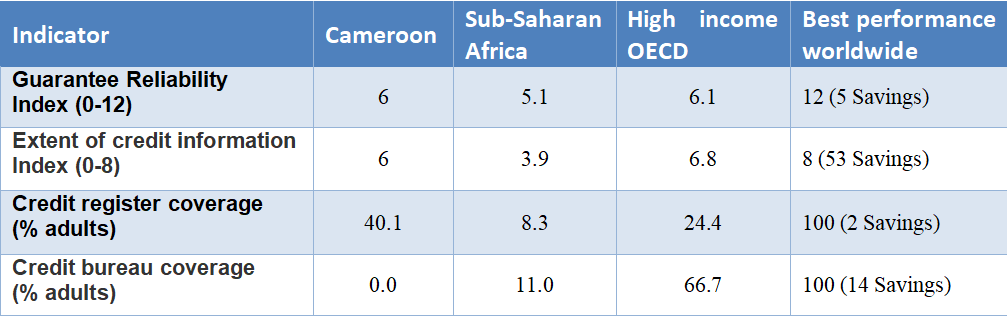

Indeed, despite Cameroon’s good performance on three of the sub-components of the loan-granting indicator, where it outperforms the average for sub-Saharan Africa and even the OECD average for credit bureau coverage, Cameroon scored zero on credit bureau coverage, while the average for sub-Saharan Africa is 11 (out of a maximum of 100).

This result is indicative of the persistence of certain institutional constraints that, according to the Doing Business 2020 report, affect the Cameroon economy. This result is indicative of the persistence of certain institutional constraints that, according to the Doing Business 2020 report, affect the Cameroon economy. This paper takes an investigative look at these constraints. Although focusing on the Cameroon Diaspora, the paper will deal with investment by foreigners, given that citizens of the Diaspora, while having retained their nationality, live their daily lives abroad.

Constraints to access to credit by foreign investors

One of the constraints to access to credit by foreign investors is the viscosity of the conditions for opening a commercial account. Indeed, the process of opening a commercial or business account, a mandatory step for both nationals and foreigners, requires the company to submit several administrative and fiscal documents, the number of which varies between 7 and 10 depending on the financial institution (FI). These require an initial deposit of up to CFAF 405,000 for sole proprietorships and CFAF 950,000 for limited liability companies (SARL) and joint stock companies (SA).

Another constraint is the reluctance of FIs to finance start-ups. This reluctance is explained by the fact that FIs base their credit risk analysis mainly on the financial statements of the companies. This includes documents such as the tax and statistical return (TSR), which start-ups can only produce after at least one year of existence.

In addition to the challenges mentioned above, there is also the challenge of lengthening the time it takes for businesses to obtain credit. Despite the willingness expressed in March 2015 by the Cameroon government, the Bank of Central African States (BEAC) and the International Finance Corporation (IFC) to create a credit bureau to facilitate access to bank financing for foreign companies, FIs still rely mainly on internal analyses to study the solvency of companies and businesses. Among other things, they check the accounting records of foreign companies to assess their credibility, and ensure their ability to repay their loans. The absence of a credit bureau is a handicapping factor for the economy of Cameroon, in particular for its financial sector. To this end, in order to encourage foreign direct investment, it is necessary for Cameroon to put in place general, transparent and favourable conditions for investment, and to strengthen human and institutional capacities (OECD, 2002).

Overcoming constraints on access to bank credit by foreign investors: policy recommendations

The zero-score recorded by Cameroon on the assessment of its credit bureau coverage calls for the urgent establishment of private credit bureaus. This initiative must be taken by the private sector – both financial and non-financial companies – in collaboration with the state, and in the framework of a public-private partnership. Therefore, institutions such as GICAM (Groupement Inter-Patronal du Cameroun), in collaboration with the state, should create a system of harmonisation and information sharing, which requires the production of useful databases for the information of foreign investors.

Cameroon can work to shorten the time it takes for its major banks to grant credit. The example of countries like Kenya, Malawi, Nigeria and Rwanda, which are doing better in this area, shows that this is possible. Cameroon can draw inspiration from their experience, where the delay is one week.

Dr. Joel M. MOUDIO is a political scientist and a researcher on public policies, political economics and public administration. He is an economic policy, governance and regional integration analyst at the Nkafu Policy Institute.

Leave A Comment